Economic plans and a budget summary for 2019-2020

The government plans to further strengthen the economy, with a forecast surplus of $7.1 billion dollars, this being the first surplus in over a decade. Small business owners, middle and low income earners and individual taxpayers all benefit from this year’s budget.

A few changes have also been made to superannuation fund measures. An increased focus on tax-avoidance and subsequent measures to prevent this is a main theme of the 2019-2020 budget.

Individuals

One-off Energy Assistance payment

As announced by the Treasurer on 31 March, the Government will provide a one-off Energy Assistance Payment of $75 for eligible singles and $125 for eligible couples to help with energy and cost of living expenses. The payment will be exempt from income tax and will be paid automatically before the end of the current financial year, subject to the passage of legislation.

Eligibility for the payment will be restricted to Australians receiving Government support in the form of the Age Pension, Disability Support Pension, Carer Payments, Parenting Payment Single recipients and veterans and dependents receiving eligible payments from the Department of Veteran’s Affairs.

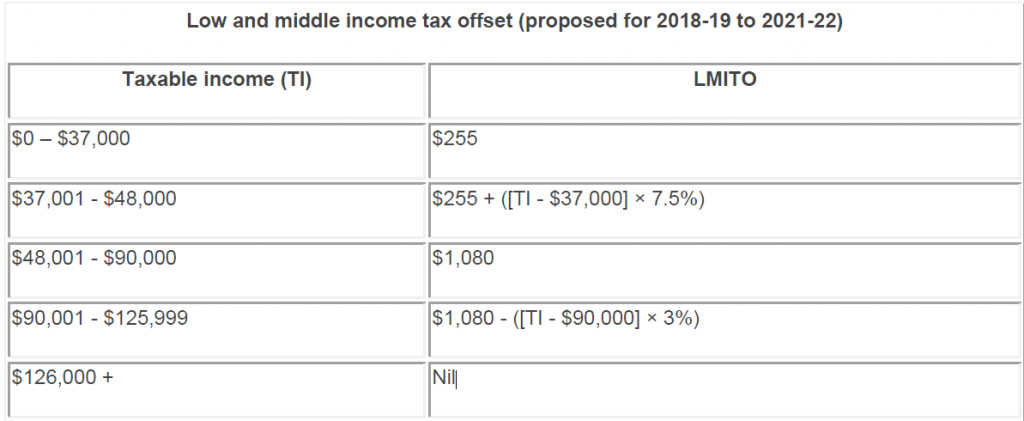

Increasing the low and middle income tax offset (LMITO) and low income tax offset (LITO)

For low and middle income earners, from 2018-19 to 2021-22, the non-refundable low and middle income tax offset will increase from a maximum of $530 to $1080 per annum, while the base amounts increase from $200 to $255 per annum. Furthermore, from 1 July 2022, the low-income tax offset, will be increased from $645 to a maximum of $700.

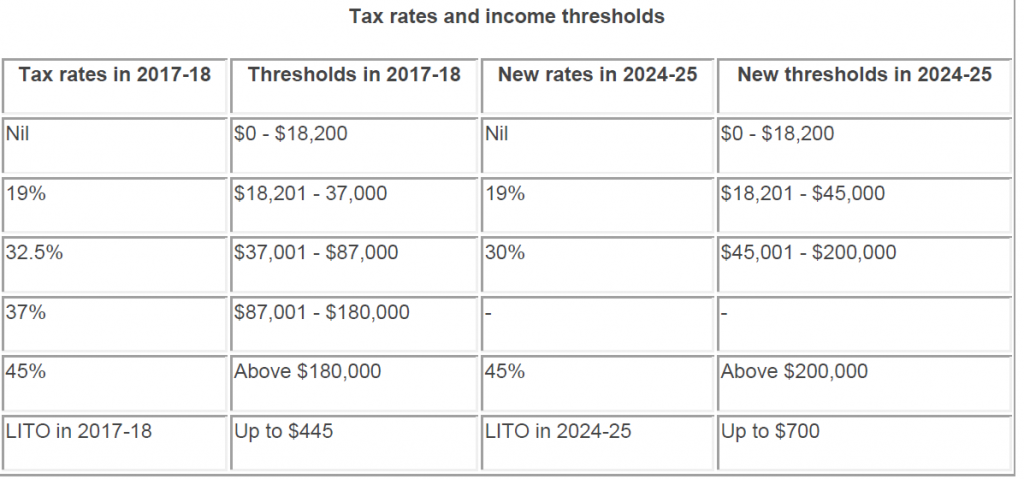

Changes to personal income tax thresholds

From 1 July 2022, the Government will increase the top threshold of the 19 per cent personal income tax bracket from $41,000, as legislated last year, to $45,000.

From 1 July 2024-25, the Government will reduce the 32.5 per cent marginal tax rate to 30 per cent. This will more closely align the middle tax bracket of the personal income tax system with corporate tax rates.

The changes are reflected in the table below:

Increasing the Medicare Levy low income thresholds

While the Medicare Levy will remain at 2% of taxable income, the Medicare Levy low income threshold will be increased for singles, families, seniors and pensioners from the 2018-2019 income year.

CGT main residence exemption changes

Despite pre-Budget speculation, there was no clarification in the Budget about the proposal to remove the CGT main residence exemption for foreign residents. Accordingly, it appears to remain Government policy, though not yet legislated.

Business Taxation

Company tax rate remains unchanged

Company tax rates have remained unchanged, with eligible companies (corporates with an aggregated turnover of less than $50 million), continuing to have a 27.5% tax rate in the 2019-20 income year, a 26% tax rate in the 2020-21 income year and a 25% tax rate in the 2021-22 income year and all following years. Other companies will also remain at a 30% tax rate for all following income years.

Expansion of STP data program

The Single Touch Payroll (STP) data program will receive further funding from the government, who from 2019-20, plan to provide $82.4 million over four years to the ATO and Department of Veteran’s Affairs. This is intended to aid in expanding data collected through STP by the ATO and Commonwealth agencies use of this data.

Increased funding for the Tax Avoidance Taskforce

From 2019-20 the Government will provide $1 billion over four years from 2019-20, including $6.5 million in capital funding, to the Australian Taxation Office (ATO) to extend the operation of the Tax Avoidance Taskforce.

This measure will allow the Taskforce to expand its compliance activities targeting multinationals, large public and private groups, trusts and high wealth individuals, including increasing its scrutiny of specialist tax advisors and intermediaries that promote tax avoidance schemes and strategies.

This measure is estimated to raise tax liabilities of $3.6 billion over the forward estimates period, and $2.0 billion in cash collections over the same period.

The Government has also provided $24.2 million in 2018-19 to Treasury to conduct a communications campaign focused on improving the integrity of the Australian tax system.

Electronic invoicing adoption

The Government will also provide $1.3 million to the ATO in 2019-20 to establish a Pan-European Public Procurement On-line Authority, which is an e-invoicing framework that is already being used across 32 countries.

Improving audit quality

The Government plans to provide $0.8 million to the Auditing and Assurance Standards Board (AASB) over three years, beginning 2019-2020, which is intended to improve audit quality in Australia by increasing support for the Financial Reporting Council’s Audit Quality Action Plan. The ATO will also receive $1 billion over four years, from 2019-20, which will go towards the Tax Avoidance Taskforce. This intends to give the Taskforce the ability to expand its compliance activities, with an emphasis on multinationals, large public and private groups, trusts and high wealth individuals, alongside increasing focus on specialist tax advisors and intermediaries which promote tax avoidance schemes and strategies. The effect of this is an estimated rise in tax liabilities of $3.6 billion, as well as $2.0 billion in cash collected over the forward estimates period.

Increased funding for debt collection

$42.1 million over four years will be provided by the Government to the ATO to increase their focus on larger businesses and high wealth individuals in recovering unpaid tax and superannuation liabilities in order to ensure on time payment of these. Small businesses will not be affected by this measure.

Black economy

Further to this crackdown on tax avoidance, from 1 July 2021, ABN holders with an income tax return obligation must lodge their income tax return. Furthermore, from 1 July 2022, ABN holders are required to confirm the accuracy of their details on the Australian Business Register annually.

Increased funding for regulators

Further funding in the form of $404 million over four years to ASIC and $145 million to APRA will be provided by the Government, to enable further investigation into aspects of the Financial Services Royal Commission.

This funding is intended to support the Federal Court in expanding their jurisdiction to include corporate crime, as well as the appointment of additional judges, registry and support staff and construction of new court facilities.

It is intended for the cost of this to be partially offset by revenue received through ASIC’s industry funding model and increases in the APRA Financial Institutions Supervisory Levies as well as from funding already provisioned in the Budget.

R&D Tax Incentive

Regarding the research and development tax incentive, no further changes were made to the Government’s policy.

Small and Medium Businesses

Extension of the Instant Asset Write-off

One of the more significant changes for small (businesses with an aggregated turnover of less than $10 million) and medium businesses (Businesses with an aggregated turnover from $10 million to $50 million) is that they will now be able to instantly write off assets up to $30,000, beginning from 2 April 2019 to 30 June 2020. This threshold applies on a per asset basis, enabling multiple assets to be instantly written off.

Small businesses are permitted to continue placing asset which cannot be immediately deducted into the small business simplified depreciation pool and depreciate these assets at 15 percent in the first income year and 30 percent each income year afterward.

Medium businesses will also continue to depreciate assets which cannot be immediately deducted, costing $30000 or more, in accordance to the currently existing depreciating assets provisions of the tax law.

Small business assistance in respect of tax disputes

In a series of announcements over the past few months, the Government has proposed the establishment of small business assistance as follows:

- A small business concierge office within the Australian Small Business and Family Enterprise Ombudsman to simplify and resolve tax disputes

- The creation of a small business taxation division within the AAT

- A review of the Scheme for the Compensation for Detriment Caused by Defective Administration (CDAA scheme) to consider the operation by the ATO of the scheme in relation to small business

- A review into the ATO’s practices in pursuing early recovery of tax debts from small businesses who are in dispute with the ATO

Export Market Development Grants

The Government will provide $61 million over three years from 2019-20 to support Australian businesses to export Australian goods and services to overseas markets, comprising:

- $60 million over three years from 2019-20 increased in funding for the Export Market Development Grants scheme to boost reimbursements levels of eligible export marketing expenditure for small and medium enterprise exporters

- $1 million in 2019-20 to further promote Australian export industries to overseas markets

Superannuation

Permanent tax relief for merging superannuation fun

The current tax relief available for superannuation funds, where revenue and capital losses can be transferred to a new merged fund, which was set to expire on 1 July 2020, has been made permanent by the Government.

A few changes have also been made to increase the flexibility of super arrangements:

- Work test exemption for recent retirees: Starting July 1 2020, Australians aged 65 and 66 will be able to make voluntary superannuation contribution, both concessional and non-concessional, without meeting the Work Test, which is a change from the current restriction by the Work Test for those aged 65-74 to make voluntary contributions unless they work a minimum of 40 hours over a 30 day period. This change will streamline the Work Test with the Age Pension eligibility age which is currently schedules to reach 67 from 1 July 2023.

- Bring forward arrangements: Australians aged 65 and 66 will now be eligible for bring forward arrangements, which allows three years’ worth of non-concessional contributions to be made up in a year. This was previously only available for individuals under the age of 65, with a total superannuation balance of less than $1.6 million.

- Age limit for spouse contributions: The age limit for spouse contributions, where contributions can be made by an individual on behalf of another, will be also be increased from 69 to 74 years.

Reducing red tape for superannuation funds

Superannuation fund trustees, with interest in both the accumulation and retirement phases during an income year, will also be allowed to choose their preferred method of calculating exempt current pension income (ECPI) from 1 July 2020. The requirement for superannuation funds to obtain an actuarial certificate when calculating ECPI using the proportionate method will also be removed, given that all members of the fund are fully in the retirement phase for all of the income year.

Reducing costs for super industry by including superannuation release authorities in electronic SuperStream Rollover Standard

$19.3 million will be provided to the ATO over three years starting 2020-21, to send electronic requests to superannuation funds for the release of money required under a number of superannuation arrangements. This will take effect from 31 March 2021.

This change will be put into action by expanding the electronic SuperStream Rollover Standard currently used for the transfer of information and money between employers, superannuation funds and the ATO. Subsequently, the start date of Self-Managed Superannuation Funds rollovers in SuperStream will be postponed until 31 March 2021, in order to coincide with the planned expansion of the SuperStream Rollover Standard.